As residents of beautiful British Columbia, you work hard to accumulate assets and build a thriving life. But amidst the spectacular landscapes, liability risks loom large. As your proud protector and educator, Stratis Insurance is here to explain the vital role of Umbrella Insurance—the extra layer of security that shields your hard-earned financial future.

What is Umbrella Insurance?

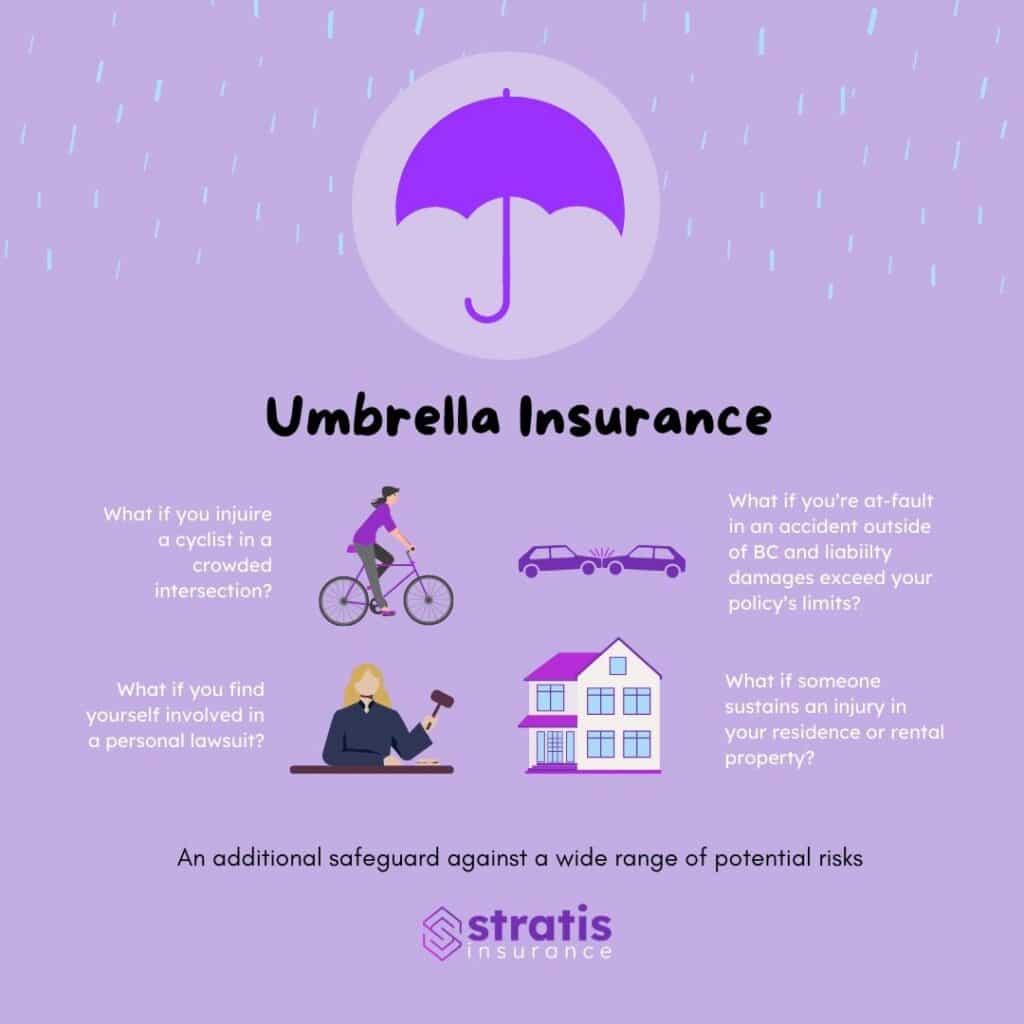

Umbrella insurance, also known as excess liability insurance, serves as supplemental coverage that extends far beyond the limits of your primary policies.

In simple terms, if a lawsuit results from an at-fault incident and the resulting damages (medical bills, legal fees, lost wages) exceed the liability limits on your standard Home or Auto insurance, the umbrella policy steps in to cover the excess amount. It is designed to safeguard your assets from catastrophic legal action.

- Coverage Limits: Umbrella policies typically offer substantial coverage, often ranging from $1 million to $5 million or more.

- Broad Protection: Coverage extends to a wide range of liability risks, including personal injury, property damage, and non-physical damages like libel, slander, and defamation.

- Legal Defense Costs: Umbrella insurance also covers the significant costs of legal defense, ensuring you have the resources to hire a competent attorney.

- Worldwide Coverage: Many policies provide worldwide protection, even when you travel outside of B.C. or Canada.

Why BC Residents Need This Extra Layer of Protection

In B.C., a unique combination of factors makes umbrella insurance a valuable, if not essential, asset:

- High Asset Vulnerability: B.C. consistently ranks as one of the most expensive provinces in Canada. Many residents have substantial assets (home equity, savings, investments) that are exposed to financial ruin if a major lawsuit occurs.

- Active Lifestyle Risks: B.C.’s natural beauty encourages an active outdoor lifestyle (skiing, hiking, boating, hosting parties). These activities, while enjoyable, come with inherent risks that increase the chance of an accident or injury occurring off-premises.

- Entrepreneurial & Social Risks: Whether you own a business, invest in properties, or simply enjoy hosting social gatherings, these activities can sometimes lead to unforeseen accidents or lawsuits, potentially exposing your personal wealth.

High-Risk Scenarios: Where Primary Policies Fail

To truly appreciate the significance of umbrella insurance, consider scenarios where standard policies, even those with high limits, are easily overwhelmed:

- Catastrophic Car Accident: You are found at fault for a serious accident causing devastating, life-long injuries to another party. Medical, rehabilitation, and lost wage costs quickly accumulate to a significant sum, easily exceeding your Auto policy limit of $1 million. The umbrella policy then covers the excess amount, potentially safeguarding your home and life savings from the judgment.

- Home Liability (Slip-and-Fall): A guest slips and falls at your home during a gathering, sustaining a major, permanent injury. They decide to sue you for medical expenses and pain and suffering that exceed the liability coverage of your Homeowners policy. The umbrella policy steps in to cover costs that exceed your Homeowners insurance coverage.

- Social Media Mishap: You post a comment on social media that unknowingly defames or slanders someone, leading to a lawsuit. Your umbrella policy can provide protection against the legal defense expenses and settlement costs associated with non-physical personal injury claims.

Selecting the Right Umbrella Policy

Umbrella insurance is known for its affordability relative to the enormous protection it offers. However, selecting the right policy requires careful assessment:

- Determine Your Coverage Limit: Assess your total assets and potential risks to determine an appropriate coverage limit.

- Maintain Primary Coverage: Most umbrella policies require you to maintain a minimum level of coverage on your primary policies (Auto and Homeowners).

- Customization: If you have unique risks, such as business ventures, discuss them with an insurance professional to ensure your policy addresses your specific needs.

Don’t wait until a costly lawsuit threatens your financial security. Get the peace of mind you deserve. Contact our team at Stratis Insurance to help you understand your unique risks and find the right umbrella policy to protect your future in B.C..