Small business life insurance in Canada is one of the most important tools entrepreneurs can use to protect their company, partners, and family. Whether you run a family business, partnership, or corporation, the right life insurance strategy helps ensure continuity, stability, and long-term success if the unexpected happens.

At Stratis Insurance, we act as your thought partner to ensure that your business is protected with the same excellence you used to build it. Small business life insurance in Canada is a strategic financial tool that safeguards operations, preserves value, and ensures a smooth transition for your successors.

1. Funding Buy-Sell Agreements with Life Insurance

A buy-sell agreement is a legally binding contract that outlines how a partner’s share of the business will be reallocated if they pass away. Life insurance is the most cost-effective way to fund these agreements, providing the immediate liquidity needed to buy out a deceased partner’s interest.

- Cross-Purchase Agreements: Each business owner buys and owns an insurance policy on the other partners.

- Entity-Purchase (Stock Redemption): The business entity itself purchases a policy for each owner.

- The Benefit: Surviving partners maintain control of the company, while the deceased partner’s family receives fair market value for their shares tax-free.

2. Key Person Insurance for Canadian Businesses

Every business has indispensable individuals whose knowledge or skills are vital to success. Key person insurance is a policy owned by the company that provides a financial buffer if a critical leader or specialist passes away.

- Replacing Revenue: Offsets lost income from sales or delayed projects.

- Recruitment & Training: Provides capital to find and upskill a suitable replacement.

- Debt Protection: Ensures that business loans or lines of credit can be repaid immediately, maintaining investor and lender confidence.

3. Estate Planning and Estate Equalization for Business Owners

For family-owned businesses, estate planning becomes complex when some heirs are involved in the business while others are not.

- The Fairness Gap: If one child inherits a $5M business, how do you provide an equivalent inheritance to their siblings?

- Liquidity for Taxes: Life insurance provides the tax-free funds needed to cover capital gains taxes triggered upon death, preventing the forced sale of business assets.

- Equitable Distribution: You can leave the business to the active heir and provide a life insurance payout of equivalent value to the other heirs.

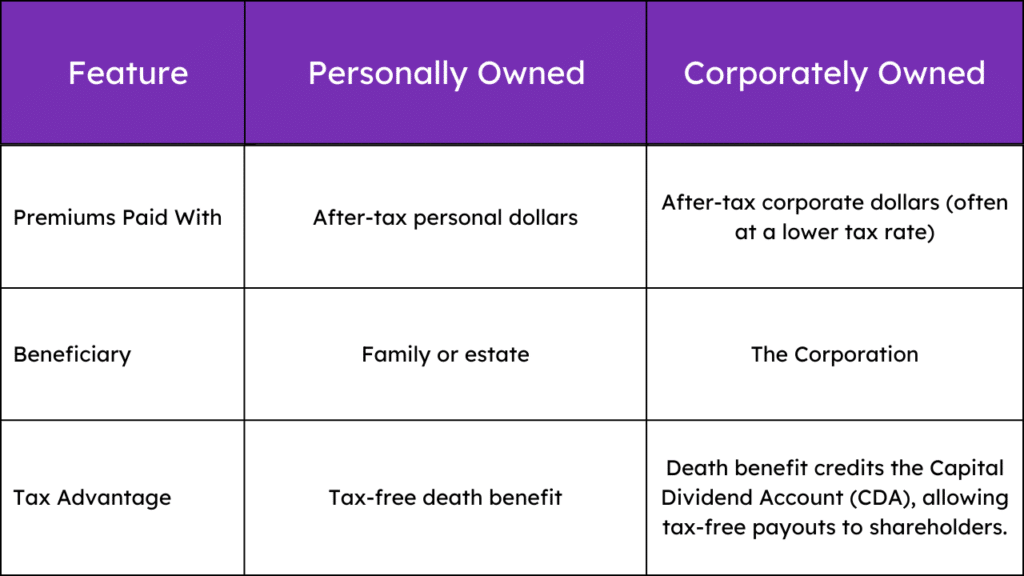

Corporate vs. Personal Life Insurance Ownership in Canada

In Canada, deciding whether to own your policy personally or inside your corporation is a critical choice.

Corporately owned life insurance can also serve as a “corporate tax shelter,” allowing for tax-sheltered wealth accumulation within the policy that can be accessed for future business growth or retirement income.

Protecting Your Life’s Work

Being a proud protector of your business means we are looking beyond day-to-day profitability and planning for long-term stability. Whether you are just starting or preparing for succession, the right life insurance strategy ensures your legacy continues exactly as you intended.

FAQ

What is small business life insurance in Canada?

Small business life insurance is coverage designed to protect a company and its owners by funding buy-sell agreements, replacing key individuals, and providing tax-efficient estate planning liquidity.

Who should own a business life insurance policy?

Policies can be owned personally or corporately. The best structure depends on tax strategy, shareholder agreements, and long-term business goals.

Is life insurance tax deductible for businesses in Canada?

Premiums are generally not tax deductible, but the death benefit is typically received tax-free. Certain structures may create additional tax advantages.

How much life insurance does a business owner need?

Coverage amounts should reflect company valuation, debt obligations, key person exposure, and estate planning needs.

Like the article? Share it with your friends!