As we enter 2026, the Canadian insurance landscape continues to offer diverse ways to secure your family’s future. One of the most common questions our clients ask is: “Should I choose term or permanent life insurance?” At Stratis Insurance, we believe that providing high-quality service starts with clear education so you can build a protection plan with excellence.

The “best” policy is not a one-size-fits-all solution; it is the one that aligns with your specific goals, budget, and stage of life.

Term Life Insurance: Affordable Protection for Key Life Stages

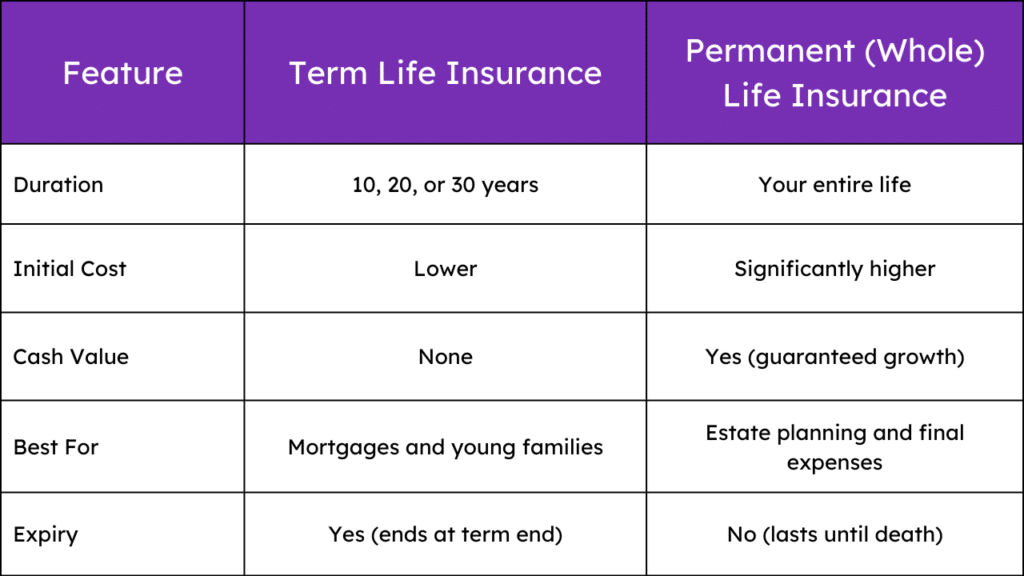

Term life insurance is often called “pure protection”. It provides a tax-free death benefit to your beneficiaries if you pass away during a specific time period, such as 10, 20, or 30 years.

- Affordability: In 2025, term insurance remained the most budget-friendly option, with premiums for healthy individuals under 40 often costing less than $30 per month for $500,000 in coverage.

- Flexibility: You can match the term length to your largest financial obligations, such as the 25 years remaining on your mortgage or the 15 years until your children finish university.

- Simplicity: The contract is straightforward—you pay a fixed premium, and in return, your family is protected for the duration of the term.

- The Trade-off: Coverage is temporary; if you outlive the term, the policy expires without a payout.

Permanent Life Insurance: Lifelong and Guaranteed

Permanent insurance (including whole life and universal life) is designed to last your entire lifetime, as long as premiums are paid.

- Lifelong Security: Your policy never expires, ensuring your beneficiaries receive a payout regardless of when you pass away.

- Cash Value Accumulation: Many permanent policies include a savings component that grows tax-deferred over time, which can be accessed for future needs like retirement or emergencies.

- Fixed Premiums: While higher than term rates initially, the premiums for whole life insurance typically remain level for life, protecting you from cost increases as you age.

- The Trade-off: Premiums can be 5 to 15 times higher than term insurance for the same death benefit.

2025 Comparison at a Glance

Many Canadians choose a “hybrid approach,” using an affordable term policy to cover high-responsibility years (like raising kids) and a smaller permanent policy for lifelong needs like funeral costs.

Which Foundation is Right for You?

If you are looking for the most coverage for the lowest cost to protect your family during your peak debt years, term insurance is usually the ideal choice. However, if your goal is wealth transfer, lifelong protection, or building a tax-efficient asset, permanent insurance may be the better fit.

As your proud protector, our goal is to empower you to make an informed decision that safeguards your most valuable assets: your loved ones.

Like the article? Share it with your friends!